I. Current Nickel Price Trend: Structural Support Behind the Retreat After Rapid Rise

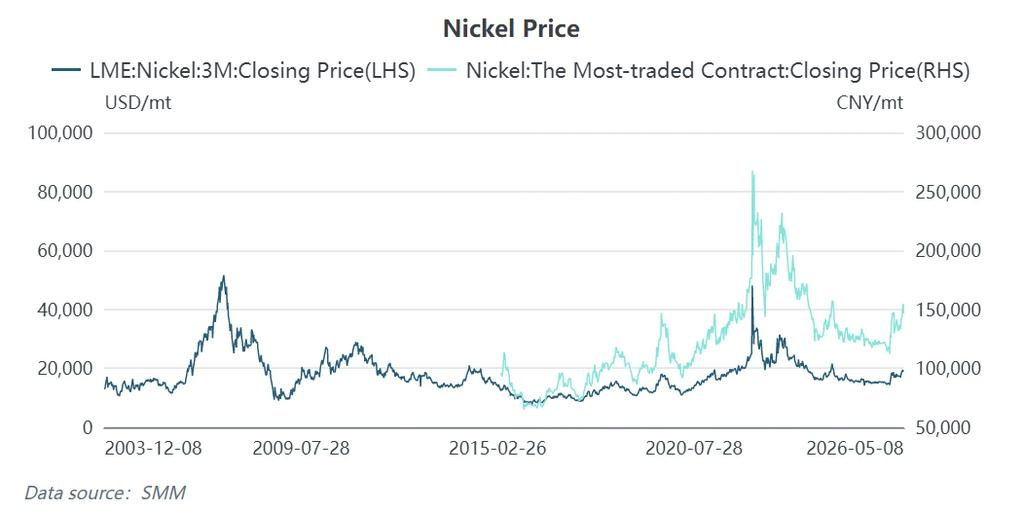

During the week ending May 8, 2026, the nickel market experienced a typical "retreat after rapid rise" — the most-traded SHFE nickel contract earlier broke through the 155,000 yuan/mt mark amid strong bullish sentiment, before quickly reversing course with a single-day decline exceeding 3%. According to SMM data, as of May 8, 2026, the LME nickel 3M closing price was $18,945/mt, and the most-traded SHFE nickel contract closed at 146,450 yuan/mt.

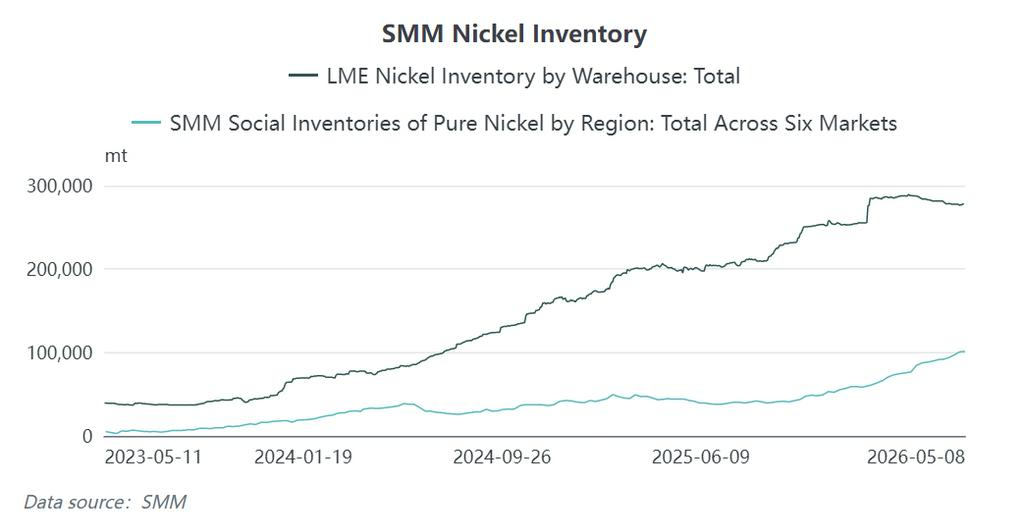

Behind the rapid pullback in nickel prices lies the most direct manifestation of the current core contradiction in the nickel market: an intense tug-of-war between strong cost support and weak physical inventory. On one hand, Indonesia's policy package combined with the sulfur crisis formed a solid cost floor; on the other hand, LME nickel inventory remained as high as 277,788 mt, still at a near seven-year historical high.

II. Sulfur Crisis: The "Fuse" and "Accelerator" of This Round of Nickel Price Rise

To understand the current logic behind nickel price increases, sulfur is an indispensable key variable. If Indonesian policies are systematically raising the long-term cost center, then the sulfur crisis ignited the market's upward momentum in the short term.

2.1 Sulfur Price Trend: A Stunning Rally from "Supporting Role" to "Leading Role"

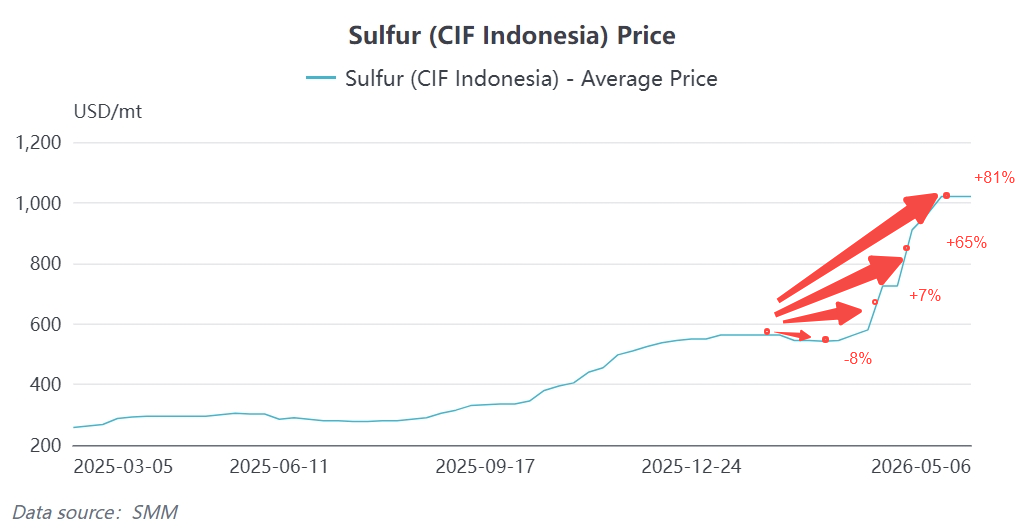

As of May 8, 2026, the SMM sulfur (solid) average price had surged to 6,928.5 yuan/mt, a cumulative increase of approximately 77% from 3,910 yuan/mt at the beginning of the year.

More critically, focusing on the Indonesian region, as of May 8, 2026, the SMM sulfur (CIF Indonesia) price had reached as high as $990–1,050/mt, with some sellers quoting prices as high as $1,250–1,300/mt. Compared to January 2026, the April average price had risen 81%.

2.2 Root Cause of the Sulfur Surge: The Strait of Hormuz "Supply Cutoff" Shock

Transmission chain:

Tensions in Iran → Strait of Hormuz blockade (starting February 28) → Disruption of Middle Eastern sulfur exports → Global sulfur supply deficit → Price surge

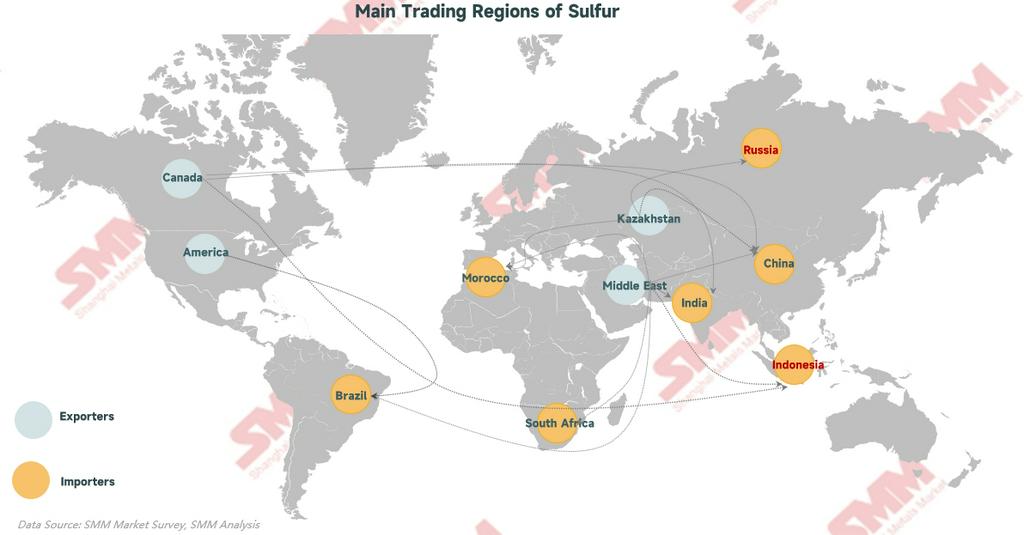

- Of global seaborne sulfur trade, 50% of cargoes originated from the Middle Eastern Persian Gulf region

- Indonesia does not produce sulfur domestically, with approximately 75% of its sulfur imports relying on Middle Eastern countries. Customs data showed that in 2025, Middle Eastern sulfur accounted for 91.6% of imported sulfur at the Obi Industrial Park and 93.9% at the IMIP Industrial Park

- Total sulfur imports of all types into Indonesia in Q1 2026 were 966,000 mt, a decrease of 420,000 mt from Q1 2025, down 30% YoY

- The extension of Russia's sulfur export ban and Turkey's export ban further exacerbated tight supply2.3 How Does Sulphur "Ignite" Nickel Prices? — A Three-Stage Transmission Path

Stage 1: Cost Surge → Hydrometallurgy Profit Collapse → Forced Production Cuts

Sulphur is a core auxiliary material in Indonesia's hydrometallurgical (HPAL) production of MHP (mixed hydroxide precipitate).

According to SMM estimates:

- Producing 1 mt in metal content of MHP requires 10-12 mt of sulphur consumption

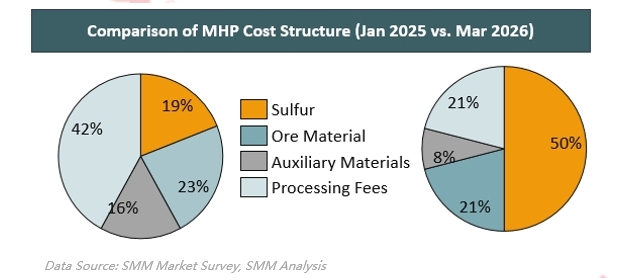

- Sulphur's share in MHP costs surged from 22% in 2022 to 50% in the current April cost structure

- Sulphur cost as a proportion of total MHP cash cost surged from 10%-30% under normal levels to 40%-60%

Landmark Event — Huafei Project Cut Production by 50%:

On April 28, 2026, Huayou Cobalt announced that its subsidiary Huafei Nickel & Cobalt would temporarily halt production and conduct maintenance on some production lines starting May 1, due to the sharp rise in sulphur prices and high-load operation of production lines, with an estimated impact of approximately 50% of production. Huafei is currently the world's largest operating nickel hydrometallurgy intermediate products project by capacity, and the news of its production cuts triggered a strong rally in nickel prices.

The sulphur crisis did not stop at Huafei alone. According to an SMM survey, other Indonesian hydrometallurgy projects also underwent maintenance or reduced load operations to varying degrees, with production impacts ranging from 15% to 50%.

Based on current market price calculations, the profit margin per mt of MHP after cobalt credit has rapidly declined from over $4,000/mt during the peak period to below $1,000/mt, with profits heavily dependent on cobalt by-products.

Stage 2: MHP Supply Contraction → Nickel Intermediate Product Shortage → Nickel Price Centre Shifts Upward

- Indonesia's MHP production was approximately 450,000 mt in 2025, with an additional 200,000 mt expected in 2026, but the sulphur shortage is disrupting this pace

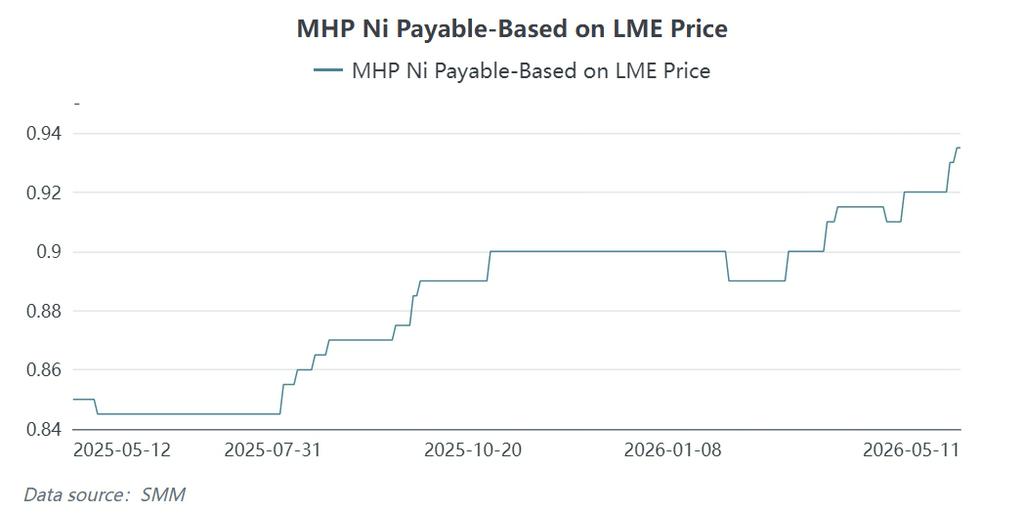

- The signal of MHP supply-side contraction is clear, with market MHP payables quoted at Ni 93.5%M / Co 92%, a notable increase from previous levels

- Strengthening MHP payables further push up nickel salt and refined nickel costs

Stage 3: Sulphur → MHP → Nickel Sulphate → Electrodeposited Nickel: Sequential Transmission

The impact of rising sulphur prices transmits sequentially along the chain of "sulphur → MHP → nickel sulphate → electrodeposited nickel." As of May 11, 2026, SMM battery-grade nickel sulphate was quoted at 34,120-34,520 yuan/mt, and SMM electrodeposited nickel was quoted at 146,900-148,600 yuan/mt. Rising costs have led to significant profit compression for hydrometallurgy projects, MHP supply contraction, and ultimately provided support for nickel prices from the supply side.

III. The Dual Overlay Effect of Sulfur and Indonesian Policies

A sulfur crisis alone might have kept the logic behind nickel price increases at the level of "short-term disruption." However, it was the overlay of the sulfur crisis with Indonesia's five-pronged policy package that formed the complete picture of this round of nickel price increases.

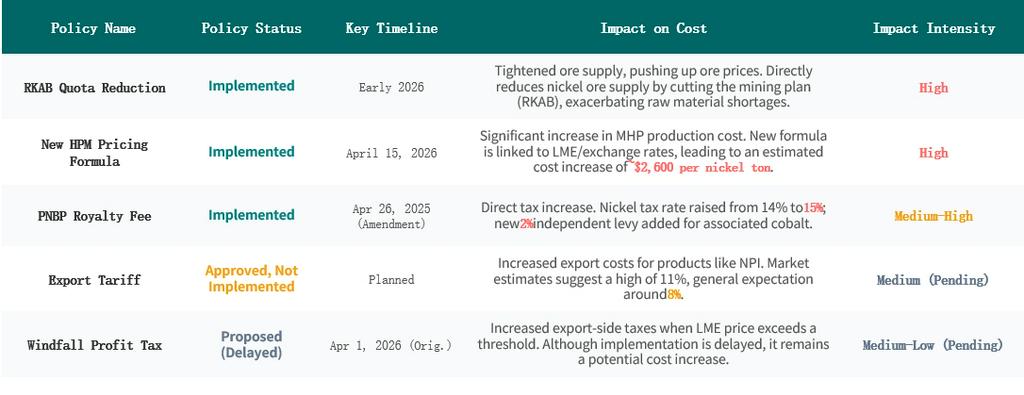

3.1 RKAB Quota Cuts: Capping Supply at the Source

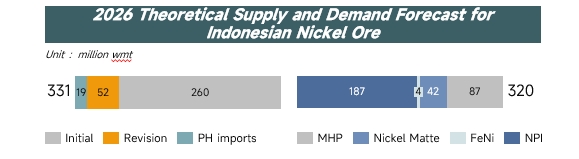

Indonesia's Ministry of Energy and Mineral Resources locked the full-year 2026 nickel ore quota (RKAB) at 260–270 million mt, a reduction of over 30% from the 2025 actual execution volume of 326 million mt. The Weda Bay mine (one of the world's largest single nickel mines) saw its quota slashed from 42 million mt last year to approximately 12 million mt, a reduction of over 70%, and entered production suspension for maintenance from mid-May onward.

This quota cut directly capped the ceiling on Indonesian nickel ore supply. At a time when the sulfur crisis was causing hydrometallurgy smelting costs to surge, the tightening of ore supply further intensified tensions and sentiment across the industry chain.

3.2 New HPM Pricing Formula: A Historic Rise on the Cost Side

If quota cuts were about adjusting "volume," then the new HPM pricing formula was about adjusting "price."

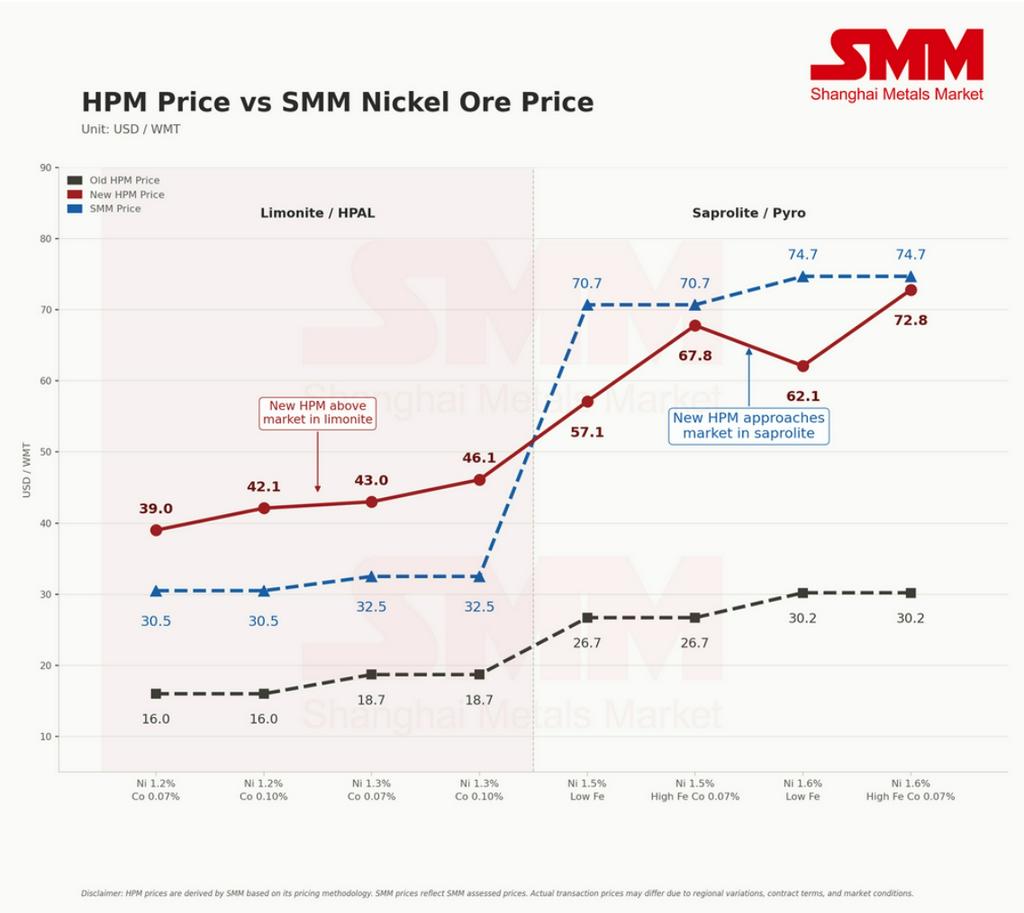

Starting April 15, 2026, Indonesia officially implemented the revised nickel ore benchmark price (HPM) calculation rules. Key changes included:

- The correction coefficient for 1.6%-grade nickel ore was significantly raised from 17% to 30% (a 76% increase)

- Co-product metals such as cobalt, iron, and chromium were included in the pricing system for the first time

- Cobalt: included when content >= 0.05%, with a correction coefficient (CF) set at 30%; Iron: included when content <= 35%, with a correction coefficient (CF) set at 30%; Chromium: correction coefficient set at 10%.

3.3 Royalties, Export Duties, and Windfall Taxes: Pending Implementation Risks

- PNBP royalty adjustment: proposed but postponed. On May 8, 2026, the Ministry of Energy and Mineral Resources held a public hearing on the revision, proposing to further refine the tax rate tiers: the minimum HMA threshold was lowered from below $18,000/mt to below $16,000/mt, and the maximum threshold was lowered from no less than $31,000/mt to no less than $26,000/mt. Based on the current nickel HMA of $17,802/mt, the applicable tax rate for nickel ore would be raised from 14% to 15%. In addition, a new independent 2% levy was proposed for cobalt in nickel matte and cobalt in non-nickel smelting products. However, Indonesia's Minister of Energy and Mineral Resources (ESDM) Bahlil Lahadalia stated on Monday that the government would suspend the implementation of the royalty adjustment plan for commodities including nickel, copper, tin, gold, and silver, in order to reformulate a more comprehensive pricing formula. Bahlil noted that the public hearing held on May 8 was merely a policy consultation phase and not a final decision; after receiving industry feedback, the government decided to "shelve" the proposal, aiming to find a balance that both optimizes state revenue and does not harm miners' interests. Although originally planned for implementation in June, the ministry will now prioritize establishing an ideal mutually beneficial model, and the timetable will be reconsidered.

- Export tariffs: According to Bloomberg, multiple officials including Purbaya confirmed that President Prabowo had officially approved export tariffs on coal and nickel, with an aggressive implementation date set for April 1, 2026. Although the specific tariff rates had not been officially announced to the public, Purbaya had previously proposed a tiered tariff scheme for coal. The scheme included rate brackets of 5%, 8%, and up to 11%, designed to dynamically adjust based on fluctuations in global market prices. The move aimed to maximize national revenue while safeguarding the competitiveness of Indonesian mineral products.

- Windfall tax: Proposed but postponed, still under discussion. Indonesia's Finance Minister stated a plan to impose a windfall tax on the nickel industry and simultaneously implement export tariffs, while offering incentives to the downstream battery industry as compensation.

3.5 Combined Effects of the Policy Package

The timeline for the systematic rollout of the five major policies is shown in the table below:

3.6 Sulfur, New HPM Policy, and PNBP Creating a "Cost Stacking Effect"

The Indonesian Nickel Smelters Association (FINI) explicitly warned that the nickel processing and refining industry may incur operational losses due to the triple increase in energy, sulfur, and HPM costs.

The Indonesian government is systematically pushing up the cost curve of the global nickel industry chain through a policy package of "volume control (RKAB quota cuts) + price increases (HPM multi-element pricing) + tax hikes (PNBP raise + export tariffs + windfall tax)."

IV. Risk Alerts and Market Outlook

4.1 Policy Implementation Negotiations Still Ongoing

It is important to note that although the new HPM policy has been implemented, the market remains in a negotiation deadlock. Due to the sudden policy change and surging costs, most smelters currently refuse to accept the new premium and insist on using the "old HPM + premium" pricing mechanism. As of early May 2026, there were no actual transactions concluded under the new multi-element formula. This means the actual cost pass-through effect remains to be observed—the outcome of negotiations between smelters and mines will directly affect the actual support level for nickel prices.

Meanwhile, the persistence of the sulfur crisis also faces uncertainties. As the Middle East situation releases easing signals and navigation through the Strait of Hormuz is put on the agenda, nickel prices may experience a periodic pullback if geopolitical risk premiums dissipate. However, in the short term, Huafei project production cuts are still ongoing, the WBN mine has transitioned to maintenance shutdown, and the tight supply pattern has not been fundamentally reversed.

4.2 Short-term and Medium-term Outlook

Short-term (Q2 2026): Cost-driven upward fluctuations

Sulfur shortage + Huafei production cuts + WBN shutdown + quota tightening—four major supply disruption factors are resonating simultaneously, providing extremely solid bottom support for nickel prices. SMM estimates the most-traded SHFE nickel contract to trade in the range of 145,000–150,000 yuan/mt. However, the "ceiling effect" from high inventory and weak demand is equally evident, and nickel prices are more likely to hold up well in a pattern of "cost floor below, demand ceiling above."

Medium-term (H2 2026): Focus on the pace of sulfur supply recovery

The core variable for nickel price trajectory going forward lies in when the Strait of Hormuz resumes navigation. If geopolitical tensions ease and sulfur supply recovers, hydrometallurgy smelting costs will pull back rapidly, and nickel prices may face periodic pullback pressure. However, even if the sulfur issue is resolved, the upward shift in the cost center brought by Indonesia's new HPM policy and RKAB quota tightening is structural and irreversible, and the nickel price floor has been systematically elevated.

Disclaimer: This report is based on the compilation and analysis of publicly available information and is intended solely for informational purposes. It does not constitute any investment advice. The nickel market is influenced by multiple factors including macro policies, geopolitics, and changes in supply and demand.

![[SMM Flash News] Indonesia Postpones Export Levy on Nickel Products to Re-evaluate Balanced Formula](https://imgqn.smm.cn/usercenter/yaAtG20251217171733.jpg)